Pearson correlation coefficient formula: r = Σ[(xi - x̄)(yi - ȳ)] / [√(Σ(xi - x̄)²) * √(Σ(yi - ȳ)²)]

Pearson correlation coefficient

Pearson correlation coefficient formula: r = Σ[(xi - x̄)(yi - ȳ)] / [√(Σ(xi - x̄)²) * √(Σ(yi - ȳ)²)]

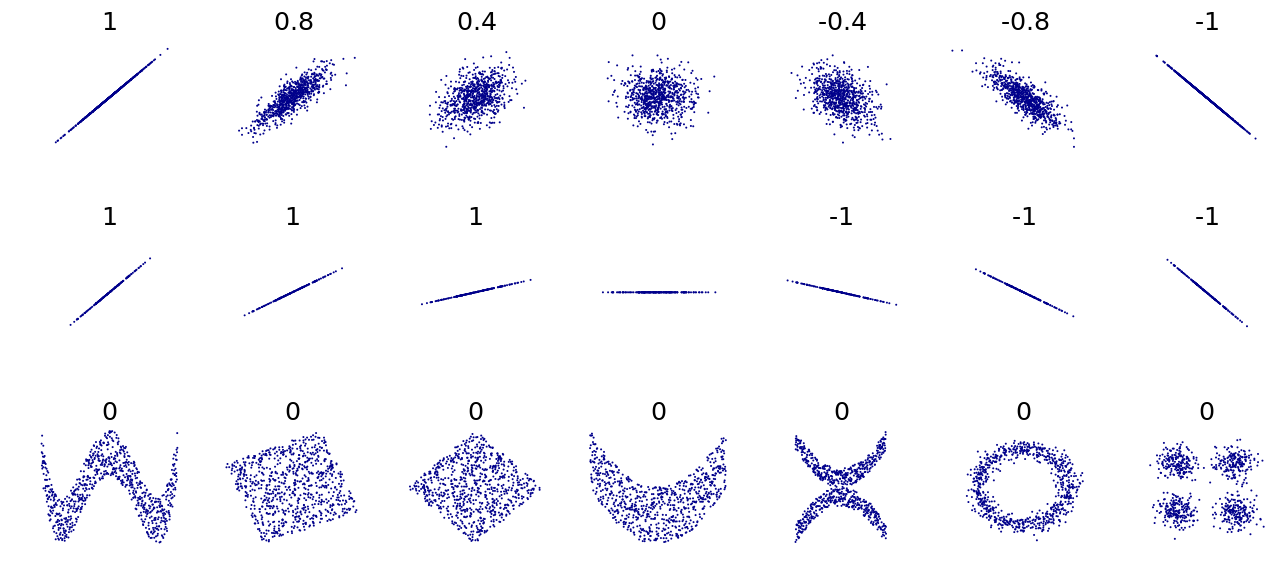

The Pearson correlation coefficient formula is a mathematical representation used to quantify the linear relationship between two variables. It is calculated by taking the sum of the product of the deviations of each variable from their respective means, and then dividing by the product of the standard deviations of the variables.

The numerator of the formula, Σ[(xi - x̄)(yi - ȳ)], represents the covariance between the two variables, which measures how much the variables change together. The denominator, √(Σ(xi - x̄)²) * √(Σ(yi - ȳ)²), normalizes this measure by accounting for the variability of each variable, ensuring the result falls between -1 and 1.

Understanding the Pearson correlation coefficient formula is crucial for analyzing and interpreting the strength and direction of linear relationships between variables in statistical studies.

Example

Consider two variables, X and Y, with the following values: X = [1, 2, 3, 4, 5] and Y = [2, 4, 6, 8, 10]. The mean of X (x̄) is 3, and the mean of Y (ȳ) is 6. The Pearson correlation coefficient (r) can be calculated as follows: r = [(1-3)(2-6) + (2-3)(4-6) + (3-3)(6-6) + (4-3)(8-6) + (5-3)(10-6)] / [√((1-3)² + (2-3)² + (3-3)² + (4-3)² + (5-3)²) * √((2-6)² + (4-6)² + (6-6)² + (8-6)² + (10-6)²)] = 1.

The Pearson correlation coefficient formula is essential for determining the strength and direction of linear relationships between variables, which is fundamental in statistical analysis and research.

Related concepts

Covariance matrix

Covariance formula: Cov(X, Y) = E[(X - E[X])(Y - E[Y])]

Standard deviation

Standard deviation (σ) is the square root of variance

Mean squared error

Mean squared error (MSE) formula: MSE = (1/n) * Σ(y_i - ŷ_i)²

Normal distribution

Normal distribution PDF formula

Expected value

Expected value formula: E[X] = Σ [x * P(x)]

Mutual information

Mutual information formula: I(X;Y) = ∑_x∈X ∑_y∈Y p(x,y) log(p(x,y)/(p(x)p(y)))

One email a day: 5 concepts + the 5 stories that matter →

Swipe through 100 ML concepts daily

Open TickerNews